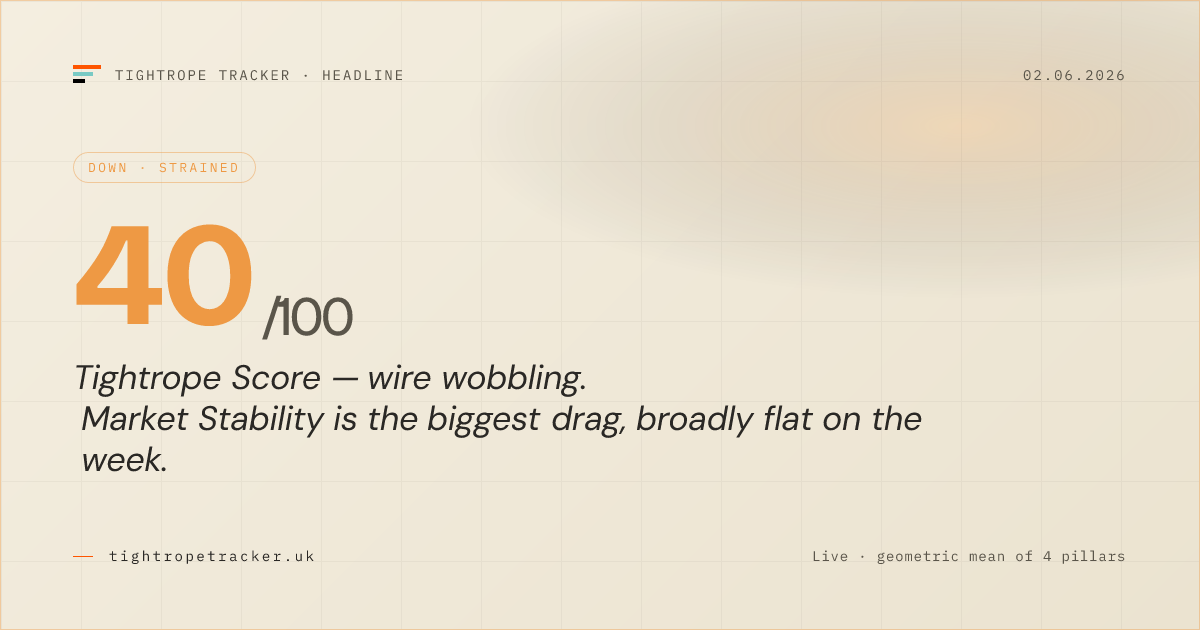

the UK is on a fiscal tightrope. the steadier the rope, the more room to move forward.

The Tightrope Score runs from 0 to 100: higher means more room to move, lower means the rope is closer to giving way. Markets, fiscal headroom, the labour force, and growth delivery each pull on the rope; the score is the geometric mean of those four pillars. Every number sourced and open.

how the score has moved

90-day headline score with the events that drove it. Hover or tab through the markers for context — every event is pinned to its primary source.

Four pillars, one score

Geometric mean · weights on each tileWhat moved today

Updated every five minutes during UK market hours. Hover any tile for the full source and timestamp.

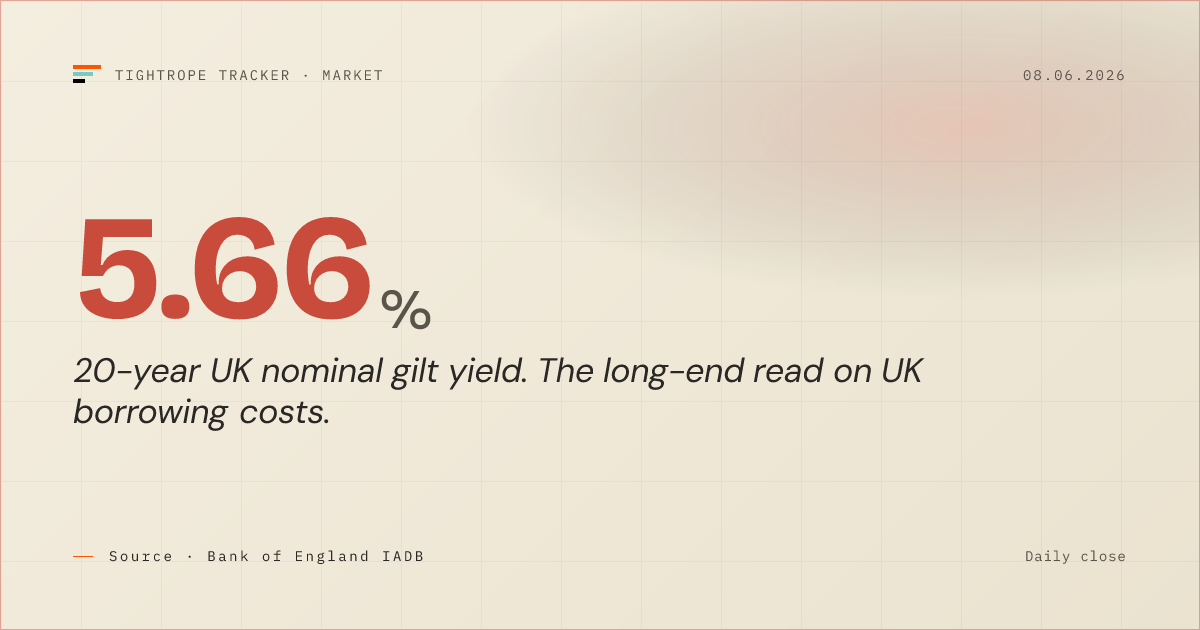

Market stability

The daily market read on UK constraint: long gilts, sterling, the rate path, mid-cap equities, and the energy input.

Gilt curve anchors

10y and 20y zero-coupon yields, breakeven inflation, and risk assets.

Market stability trajectory

30-day pillar score. Higher = more market stability; lower = more constraint from markets.

Scored 30 of 30 days.

Why this matters

Long gilt yields are the price the Government pays to borrow. When they rise, debt service bills rise with them, the Chancellor's fiscal headroom shrinks, and sterling often weakens — compounding inflation via imports. The 20-year zero-coupon yield is the clearest long-duration read on the BoE curve, and it is the one that moves first when policy credibility is in question.

Fiscal room

How much room the Chancellor actually has against her own stability rule, and how that has moved between forecast rounds.

OBR forecast headroom for FY 2029/30, by vintage

Editorial ↗£ billion, surplus against the stability rule at the FY 2029/30 target year. Each dot is a separate OBR forecast round.

The DMOUK Debt Management Office — the executive agency that issues gilts (UK government bonds) on behalf of HM Treasury. Its 'gilt stack' is the planned mix of new bonds it will sell over the financial year, by maturity bucket and type. gilt stack (forecast)

Editorial ↗Planned 2026/27 issuance · £252.1bn total · GDP = £2,709bn (OBR Spring Forecast 2026)

| Nominal | % of GDP | |

|---|---|---|

| Total issuance | £252.1bn | 9.3% |

| Short conventional | £72.1bn | 2.7% |

| Medium conventional | £81.8bn | 3.0% |

| Long conventional | £74.7bn | 2.8% |

| Index-linked | £23.4bn | 0.9% |

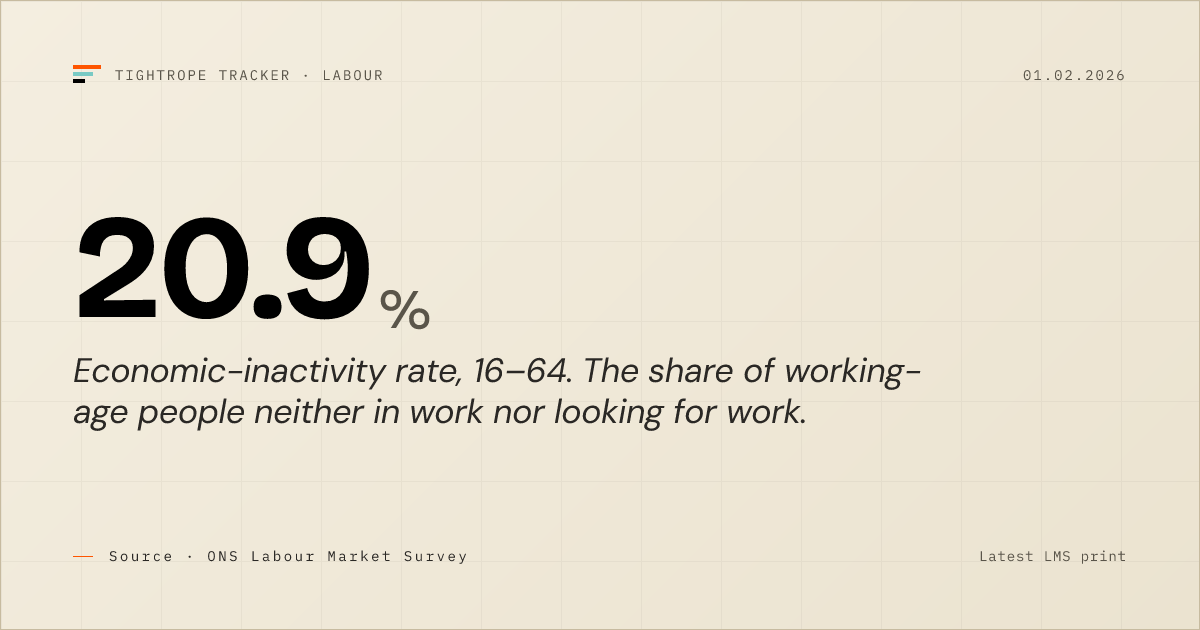

Labour & living-standards resilience

Health-related inactivity, labour-market tightness, real wages and — the line households feel — mortgage rates.

Real regular pay growth (YoY)

Editorial ↗CPIH-adjusted. Positive values = real wages growing.

Vacancies per unemployed person

Editorial ↗Rolling quarterly ratio — falling = more slack appearing in the labour market. The Tightrope methodology treats this as a worsening indicator and inverts it before it reaches the high-good pillar score.

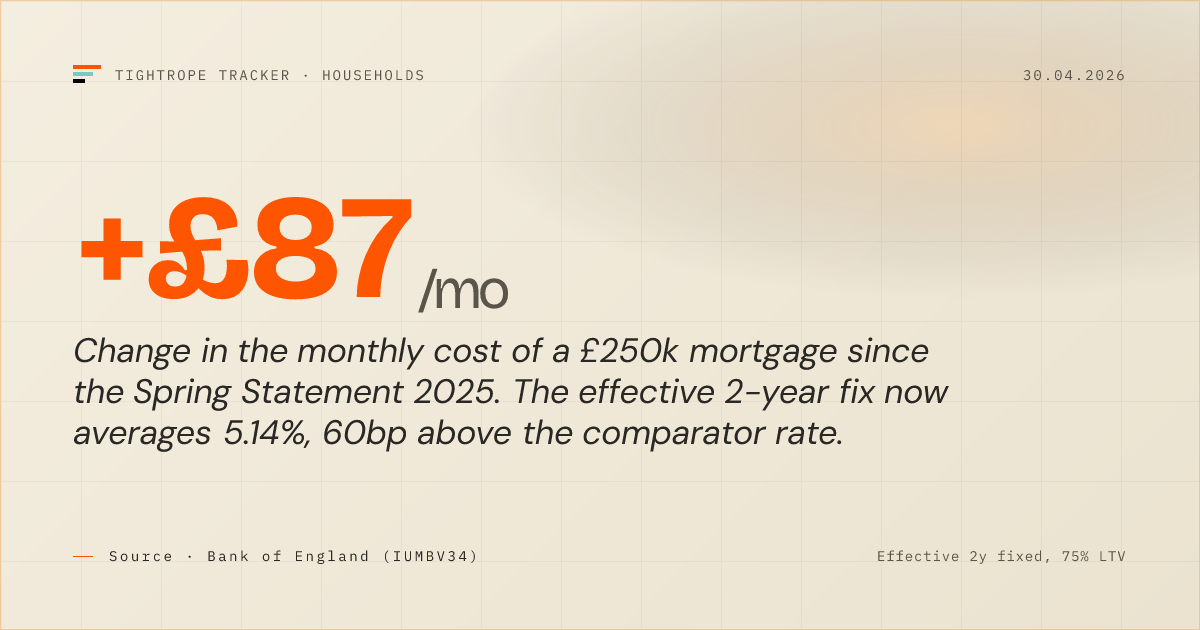

Mortgage translator

Editorial ↗What the 2-year fixed-rate move means on a £250,000, 25-year repayment mortgage.

Change vs. the rate at the Spring Statement 2025 (4.54% → 4.81%). Payment: £1,434 vs. £1,395.

This is the line you will see quoted in the press. The rate series is the Bank of England's IUMBV34 monthly effective rate on new 2-year fixes at 75% LTV · latest reading 30 Jun 2026.

Inactivity rate vs. health-related count

Editorial ↗Annual averages, 16-64. Left axis: rate (%). Right axis: health-related inactive (millions).

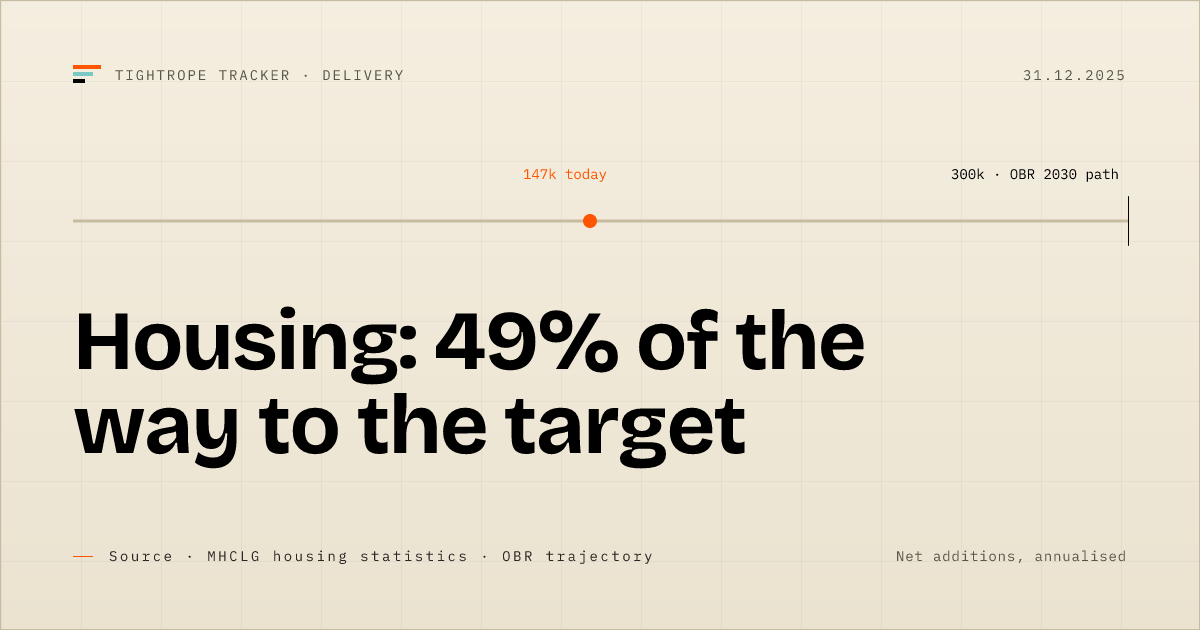

Is the Government hitting their targets?

The Government's own stated commitments, tracked against public milestones. Green for on track, amber for slipping, red for missed, blue for shipped. Every status is sourced.

The events that moved the rope

OBR forecast rounds, BoE decisions, Budget set-pieces, and the geopolitical shocks that landed in between. Pinned to primary sources.

Renewed US–Iran tensions push gilts to a four-week high

Fresh US strikes and a declaration that the ceasefire is over send crude to two-week highs and reignite imported-inflation fears. The 10-year gilt yield climbs about 10 basis points on the week to print 4.95% on 9 July — its highest in four weeks — as money markets move to price at least one Bank of England rate hike by year-end, with roughly one-in-four odds of a second. The leadership transition due mid-month keeps a domestic risk premium in the curve.

Trading Economics (market report) ↗Nigel Farage resigns his Commons seat via the Manor of Northstead

The Chancellor of the Exchequer appoints Nigel Paul Farage as Steward and Bailiff of the Manor of Northstead — the procedural mechanism by which an MP resigns their seat, as Parliament does not permit direct resignation. The Reform UK leader leaves the Commons ten weeks after his party's historic local-election gains and days before the Labour leadership contest concludes, adding a further by-election to the political calendar during the transition of power.

HM Treasury (gov.uk announcement) ↗Prime Minister announces resignation; gilts and sterling wobble, then steady

Keir Starmer announces he will resign as Labour leader and Prime Minister once a leadership election concludes, following the May local-election defeats and the Makerfield result. Markets, having largely priced the outcome, react modestly: sterling slips to around $1.32, the 10-year gilt yield prints near 4.85% intraday before easing, and attention shifts to whether the next government maintains the current fiscal rules. Nominations open 9 July with a new leader due before Parliament returns in September.

Al Jazeera (contemporaneous report) ↗May borrowing overshoots the OBR profile at £23.3bn

Public sector net borrowing comes in at £23.3 billion for May — £5.6 billion above the OBR's monthly profile, driven by higher-than-anticipated central government spending. Borrowing for the financial year to May reaches £46.3 billion against a £38.6 billion forecast. The overshoot lands in the middle of the leadership contest and sharpens the question of how much fiscal headroom survives to the autumn statement.

Office for National Statistics ↗Andy Burnham wins the Makerfield by-election

Greater Manchester Mayor Andy Burnham wins the Makerfield by-election, defeating Reform UK's Robert Kenyon and returning to the Commons; he resigns the mayoralty the following day. The contest, triggered by Josh Simons' resignation on 14 May, is widely read as positioning Burnham for a leadership challenge — four days later the Prime Minister announces his resignation.

House of Commons Library ↗Bank of England holds Bank Rate at 3.75%

The Monetary Policy Committee votes 7–2 to hold Bank Rate at 3.75%, with two members preferring a quarter-point rise. CPI inflation has eased to 2.8%, but the Committee expects it to rise later in the year as higher energy prices pass through — global energy costs have retreated since May yet remain above pre-conflict levels and volatile. The hold keeps the rate path data-dependent through an energy shock the MPC cannot look past.

Bank of England ↗Gilt yields post biggest weekly drop since 2023

Gilt yields fall the most in a week since late 2023 as the pressures of mid-May unwind together: Andy Burnham commits to the government's existing fiscal rules, betting-market odds on a leadership change recede, and oil falls on optimism over US–Iran talks. The 10-year eases roughly 30 basis points from its peak toward 4.85% — a five-week low by 26 May — and the 30-year falls over 30 basis points on the week, while traders price one fewer rate hike for 2026.

CNBC (contemporaneous report) ↗10-year gilt yield peaks at 5.14%, highest since 2008

The 10-year gilt yield peaks at 5.137%, its highest since July 2008, with the 30-year touching 5.86% — territory last seen in 1998. The sell-off combines a global rout in long-dated government bonds with a UK-specific political risk premium: a cabinet resignation the day before and open speculation about a leadership challenge revive memories of 2022's fiscal-credibility shock, and long maturities bear the brunt through higher term premia.

Reuters (via Yahoo Finance) ↗Local elections: historic Labour losses as Reform UK takes 12 councils

English local elections across 136 authorities deliver the largest gain by any party outside the big two in local-election history: Reform UK wins over 1,050 seats and control of 12 councils. Labour loses roughly 340 councillors, seven councils held since the 1990s, and finishes third in equivalent vote share for the first time. The result intensifies pressure on the government's delivery agenda and begins the sequence that ends in the Prime Minister's June resignation.

Rallings & Thrasher / LGC ↗Oil tops $118 as Hormuz blockade escalates

Brent crude rises for an eighth straight day to top $118 a barrel after the US President pledges to blockade Iran until it agrees a nuclear deal, touching $126.41 the following day — the highest in four years. With the Strait of Hormuz (normally a conduit for around a fifth of global oil and gas) effectively shut, the energy shock feeds directly into UK inflation expectations and pares back priced-in Bank of England rate cuts.

CNBC (contemporaneous report) ↗March CPI rises to 3.3%, BoE path under scrutiny

ONS releases March 2026 CPI inflation data showing headline CPI at 3.3% YoY (up from ~3.0% in February), driven by lingering energy and petrol price effects from the Iran conflict period. Markets price in a more cautious BoE path ahead of the 30 April MPC decision; gilt yields stabilise but remain elevated.

ONS Consumer price inflation ↗Resolution Foundation: conflict could erase £16bn of headroom

Resolution Foundation warns that a prolonged or severe Middle East conflict could erase up to £16bn of the Chancellor's current-budget headroom — almost three-quarters of the March OBR cushion — via higher energy prices, inflation, and debt interest. Report highlights fiscal vulnerability even under the current ceasefire.

Resolution Foundation ↗Sterling recovers to pre-war levels

GBP/USD back near 1.2400 as the Iran ceasefire holds and Strait of Hormuz shipping normalises. Oil and UK gas sell off sharply. BoE officials nonetheless stress inflation control remains the priority.

Reuters, Bank of England ↗Reeves rules out tax rises or borrowing for extra defence spending

Chancellor tells reporters additional defence outlays up to the 3.5% commitment will not be funded by more borrowing or higher taxes, pointing the pressure back at welfare and departmental restraint.

Reuters, HM Treasury ↗US, Israel and Iran agree conditional ceasefire

US, Israel and Iran agree a conditional two-week ceasefire; UK Foreign Secretary and international finance ministers welcome the de-escalation, citing restored Strait of Hormuz shipping and falling oil and gas prices. Initial market relief begins, setting the stage for sterling's recovery to pre-war levels by 17 April.

Foreign Office / gov.uk ↗OBR Spring Forecast: headroom 23.6bn, GDP cut to 1.1%

Current-budget headroom ticks up from 22.0bn at the November Budget. 2026 growth downgraded from 1.4%. IMF subsequently cuts to 0.8% citing the Middle East shock.

OBR, IMF ↗Iran conflict begins, energy shock lands

UK natural gas front-month jumps 38% inside a week. 30y gilts break 5.5% for the first time since 1998. Tightrope Score moves from 51 to 68 over four trading sessions.

ICE, Bank of England ↗BoE cuts Bank Rate to 3.75%

7-2 vote. MPC minutes emphasise inflation persistence; markets trim the 2026 cut path.

Bank of England MPC ↗Planning & Infrastructure Bill receives Royal Assent

Landmark reform of the planning system passes both houses with cross-bench support; commencement orders expected by late spring.

Planning & Infrastructure Act 2025 ↗Autumn Budget: 22.0bn headroom restored

Combination of receipts upgrade and tighter departmental envelope rebuilds the cushion after the March 2025 crunch (9.9bn).

HM Treasury, OBR ↗BoE holds Bank Rate at 4.00%, starts reducing gilt sales

QT pace pared back; MPC cites technical market conditions rather than policy loosening.

Bank of England MPC ↗Industrial Strategy white paper published

Sets out eight priority sectors and the British Industrial Competitiveness Scheme framework.

DBT ↗OBR Spring Forecast: headroom collapses to 9.9bn

The crunch. Gilts reprice and the Chancellor promises restoration in the next fiscal event.

OBR ↗First Reeves Budget: 22.0bn headroom set

Opening fiscal envelope. Employer NICs rise, capital budgets reprioritised toward infrastructure.

HM Treasury ↗what if…?

Drag any of the 14 headline drivers — gilt yields, pay growth, headroom, housing — and watch the score, pillars, and band recompute through the same empirical-CDF baseline the live methodology uses. Counterfactual, not a forecast.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Three useful things you can do with this

Join Looking For Growth

Looking For Growth is the cross-party movement campaigning to get Britain building, growing and delivering. If the numbers on this page move you, the most useful thing you can do is join the people working to change them.

Write to your MP

Enter your postcode. We'll find your MP and pre-fill a short, factual letter citing today's Tightrope Score, the pillar most affecting it, and the methodology page. One click opens a draft email to your MP's parliamentary address.

Letter copied to clipboard — paste it into the form on Parliament's site.

Want to do more than write a letter? Sign up to LFG ↑.

Embed the live score

Think tank, Substack, internal dashboard — paste one iframe. Numbers update from the same API that powers this site. No key needed. Each variant ships with its natural height baked in so the widget doesn't clip on the receiving page.